Food Inflation

Cheers to the new subscribers. I am honored you are here. Let’s change the financial future for our families and the world.

It will be a brief note today and a bit of a more practically-minded break from the philosophical focus of this Sunday note.

While so many eyes are on energy and global conflict, I’d like to call your attention to three charts.

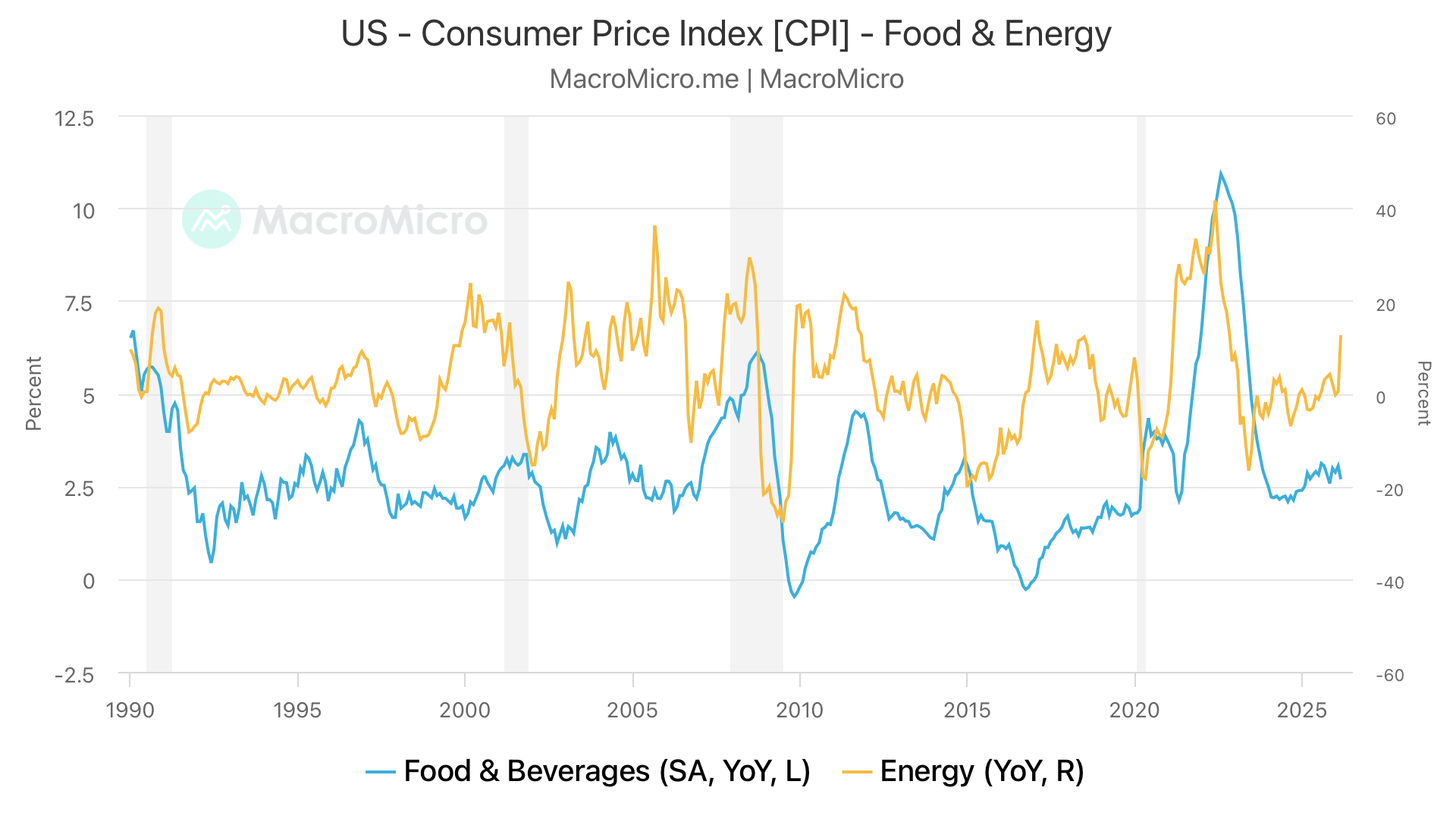

This first one shows consumer prices of energy products in yellow and food and beverages in blue. You’ll notice that large energy price changes tend to lead food and beverage price changes. Now look at the very right - at that yellow spike in energy that shows where we are now. Food is next.

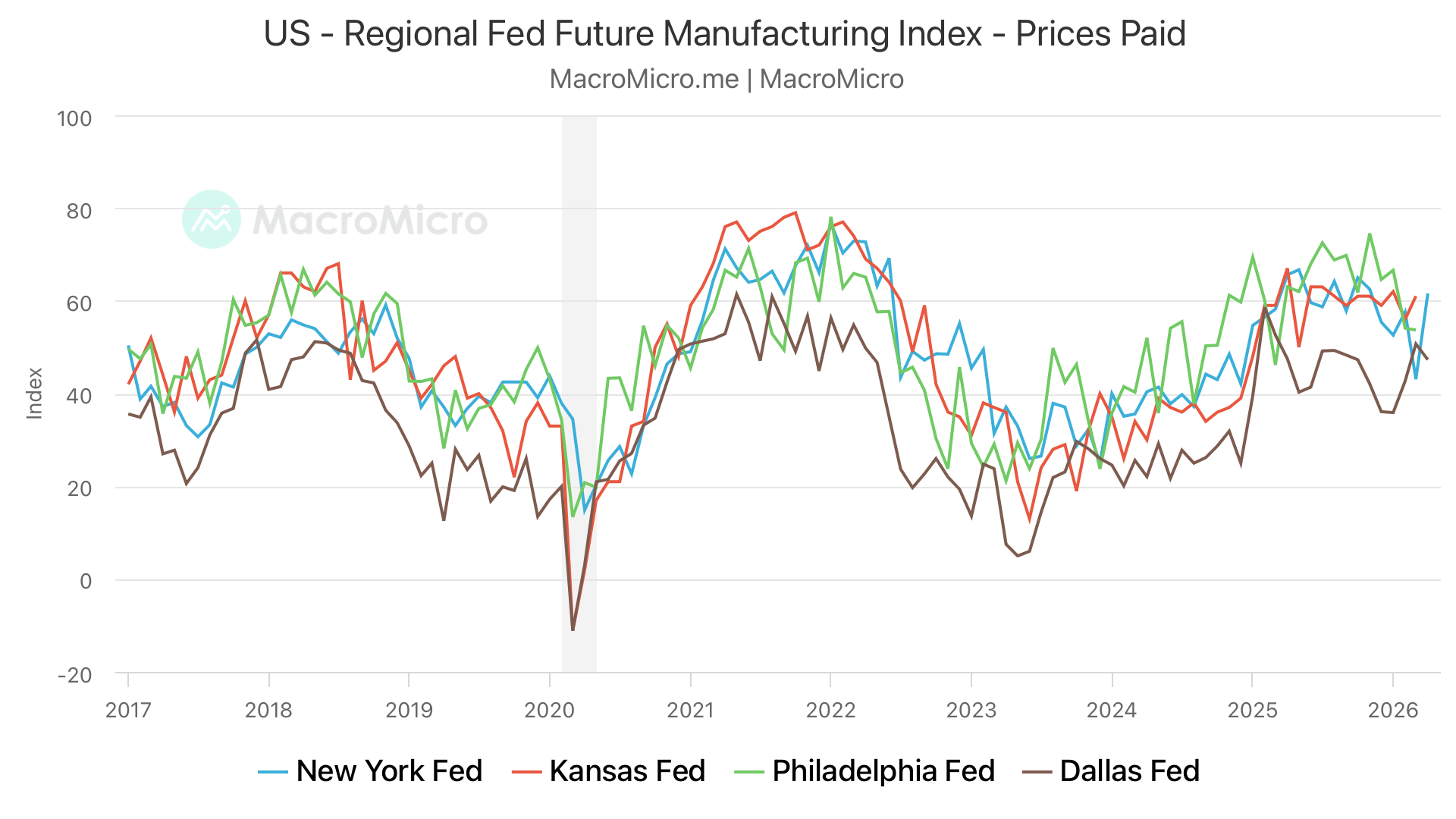

Now look at the various regional Federal Reserve Producer Prices Paid indices - these indices are based on regional business survey data, compiled by each regional Fed bank. The data is then calculated using a ‘diffusion index’ methodology where they aggregate response data using the following formula:

The percentage of business respondents that expect price increases to obtain the materials they need to produce their goods, minus the percentage of respondents that expect a decrease in prices. (These are 6-month, forward-looking expectations.)

What we see in this data since the middle of 2023 is a clear, long-term trend. Businesses across the US are expecting to pay higher prices.

You’re thinking - ok - but those are just expectations. That’s squishy data.

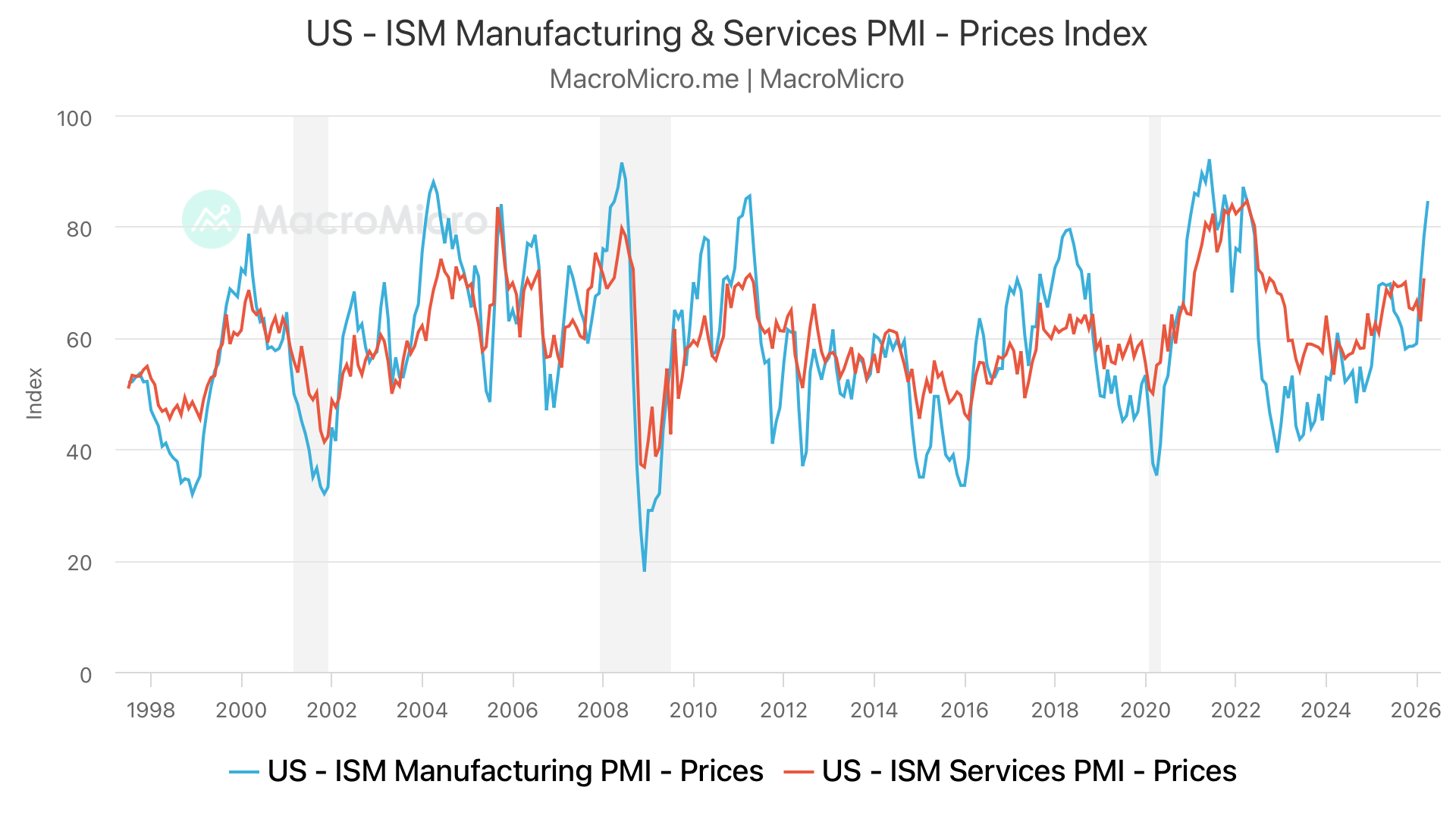

Well, here’s what producers are actually paying for manufacturing materials via the ISM (Institute for Supply Management) Producer Manufacturing ‘Prices Paid’ sub-index:

Here again, you’ll see a correlative relationship. Manufacturing prices and prices for services are highly correlated, with manufacturing prices leading the way. Note that blue spike in manufacturing at far right — where we are now. Services prices are next.

So what do we do? We turn our trading attention to food commodities and food commodity processors. We know eating is about to get more expensive, and that the dollar is becoming worth less and less. We know that the spring planting season has already been disrupted and that the crop yield effects are lagging. We know that fertilizer costs have skyrocketed due to the Straight of Hormuz trade disruption.

This is an opportunity to offset financial hardship with increased portfolio profitability. We all have the power to do this. And if you don’t want to trade yourself - that’s great - find a macro-savvy, trend-following trader (the most talented one I know is Jason Perz) and we will soon also be launching a fund of our own too.

Have a great week,

Andy